Your CPA Told You to Buy a Truck. Here's What They Missed.

How a $600,000-a-year couple cut their tax bill by $200,000 annually using a retirement vehicle most advisors have never mentioned

A few months back, a referral called our office.

They had heard we helped people save money on taxes. So, I sat down with them on a Zoom call — him and his wife, both working corporate jobs.

Between the two of them, they were clearing over $700,000 a year on W-2 income. They also had an additional $350,000 of profit coming in from various business entities.

Smart people. Successful people. Doing everything they thought they were supposed to do. Hire a CPA? Check. Working with Schwab online to save money? Check.

The problem they faced was that despite having “advisors,” they had a bunch of stuff all over the place that was not connected.

All of their “stuff” wasn’t solving the one thing killing their financial plan and peace of mind.

Taxes.

They Were Buying Things to Escape Their Taxes

Every year, their CPA had the same advice: find a deduction.

So, they did. Real estate. Businesses. Assets that depreciate. Equipment. Trucks.

The logic made sense on paper — put money into things that lose value over time, write off the depreciation, reduce your taxable income.

But there was a catch.

They had an S-Corp. And here is what happens with an S-Corp that most people do not fully appreciate until they are living it: the profit flows through to your personal tax return.

That is called pass-through income. It sounds clean in theory.

In practice, it meant every asset they bought to generate a deduction was also generating income — which flowed right back through the S-Corp onto their personal return and added to their tax bill.

They were running as fast as they could and ending up exactly where they started.

I said to them, half joking, “That sounds like a lot of my clients. Gosh, how many more trucks and equipment do you need in your front driveway?”

He looked at me through the Zoom call and said, “Are you kidding? I have a brand-new 2024 Ford F-250 sitting in my driveway that I have not driven one mile.”

That is what tax planning without a real plan looks like.

The Trap Most CPAs Don’t See

Here is why this cycle keeps happening.

When a CPA tells a high-income client to go buy a depreciating asset, they are technically correct. You get the deduction. Your taxable income drops for that year. From a pure tax filing standpoint, it works.

What it does not account for is your financial health.

The government gives you that tax break because they know what you bought. They know the truck depreciates. They know the equipment loses value.

They know you just used your own money to stimulate the economy with an asset that is going to be worth less every year you own it. That is why they are willing to share a little of the tax burden with you.

It is a short-term win built on a long-term loss.

And if your asset generates income? Now you have not solved the problem. You have compounded it.

A dollar lost in taxes is a dollar gone forever. But a dollar spent on a depreciating asset just to avoid taxes is two dollars gone — one to the asset, one you never recover.

This couple had been running this playbook for years. Buying things, they did not need because their CPA said it was the move. It was not bad advice exactly. It just was not the whole picture.

The Question That Changed Everything

Before I showed them anything, I asked one question.

“What do you know about a cash balance plan?”

They had never heard of it.

Most people have not. Their CPA had not mentioned it. Their financial planner had not mentioned it.

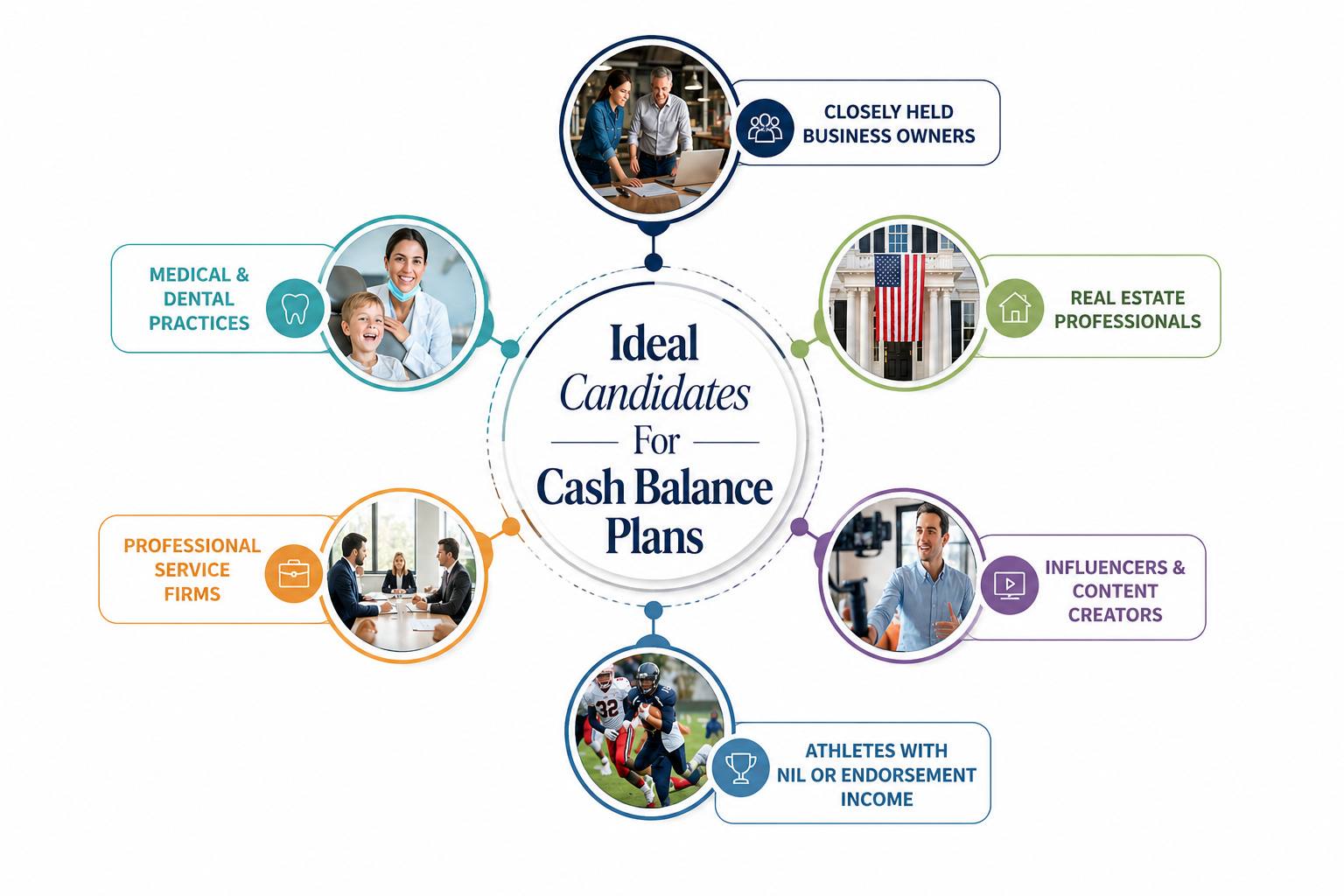

And yet, for high-earning business owners and professionals, a cash balance plan is one of the most powerful tax reduction tools available in the entire tax code.

So let me explain it.

What a Cash Balance Plan Actually Is

A cash balance plan is a pension plan. Specifically, it is a defined benefit plan — which means it is actuarially designed based on your age.

Here is what that means in practical terms: the older you are, the more you can put in.

A 401(k) has contribution limits that are the same for everyone. Right now, the maximum is around $69,000 a year including employer contributions.

For a couple earning $600,000, that is barely a rounding error. It does not move the needle on their tax bill.

A cash balance plan is a different animal entirely.

Depending on your age and income, a cash balance plan can allow you to contribute and deduct anywhere from $100,000 to more than $1,000,000 per year. Every dollar goes in pre-tax.

Every dollar reduces your taxable income. And instead of buying a depreciating asset you park in your driveway, you are building a real retirement account that grows tax-efficiently.

For this couple, we designed a plan around their S-Corp pass-through income — the income they did not need and could not get ahead of on taxes.

Instead of watching it flow through to their personal return, they redirected it into the cash balance plan.

Now it is compounding. Now it is working for them. Now the truck can stay parked.

What Business Owners Need to Know

It is designed for a window, not a lifetime.

Cash balance plans are typically funded over five to ten years. They are not like a 401(k) where you contribute steadily until you are 59. You pick a window. You fund aggressively inside that window. Then you have options.

For business owners who feel behind — who have had all their money tied up in the business and not enough set aside for retirement — this is how you catch up. We are talking about making a decade’s worth of retirement contributions in five years. Not a hypothetical. That is how these plans are designed to work.

The flexibility that makes this work.

We did a review with a different client a couple of years into the plan. He needed to fund another $200,000 that year for tax purposes, but he also had other financial commitments pressing on him.

The good news about cash balance plans is that your annual contribution has flexibility. You are not locked into the same number every year. You work with your actuary, look at your income and timeline, and determine what makes sense for that year.

And if you are a more conservative investor — if you look at stock market volatility and want no part of it — cash balance plans are designed to be invested conservatively.

They are pension plans. Conservative is the default, not the exception. You get the tax benefit without taking equity risk to do it.

The deadline is longer than you think.

Here is something most business owners miss, and it matters right now.

If you file a tax extension, you have until the extension deadline to fully fund your cash balance plan for the prior year.

At the time of this writing, we are in 2026. That means you can still fund a cash balance plan for your 2025 taxes all the way until September. If you are sitting on a tax bill from last year and wondering what you can still do about it, this window is still open.

You can solve multiple problems with one vehicle.

This is the part that surprises people most.

This couple came in with a tax problem. But as we dug into their full picture, another issue surfaced. They had a sizable net worth. And with their investment growth and the projected value of their business, their estate was on track to exceed the federal estate tax exemption.

Estate taxes on anything above that exemption — a problem they had not even started thinking about.

We folded life insurance into the cash balance plan. Through a technique called a seasoned dollar swap, we moved money out of the plan — purchased with other dollars at a discount — into a trust.

Now the same vehicle solving their short-term tax problem is also solving their long-term estate tax problem.

One tool. Two problems solved. Sometimes three or four.

That is the power of a well-designed cash balance plan. It is not just a retirement account. It is a planning platform.

If You’re a Business Owner Reading This

I want you to sit with one idea.

You cannot think your way to a lower tax bill. You cannot efficiently deduct your way there either — not if every deduction you take is generating income somewhere else.

The clients who get ahead on taxes are not the ones who bought the most stuff. They are the ones who found a qualified, tax-sheltered vehicle and funded it aggressively while the window was open.

They stopped trying to outrun the IRS and started redirecting money to a place the IRS cannot reach.

Cash balance plans are not complicated. They are just not talked about. Your CPA’s job is to file your return accurately. Your financial planner’s job is typically to manage your investments and other areas of your planning.

Very few people are sitting at the intersection of both, asking the right question: what is the most tax-efficient way to build your wealth right now?

That is the question that saved this couple over $200,000 a year in taxes over a five-year period.

Not a truck. Not a piece of equipment. Not another entity.

A plan.

Disclosures:

This blog contains general information that may not be suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this blog will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Revolutionary Wealth LLC does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance. Past performance is no guarantee of future results.

Not associated with or endorsed by the Social Security Administration, Medicare or any other government agency.

Maximizing your Social Security Benefits assumes foreknowledge of your date of death. If as an example you wait to claim a higher monthly benefit amount but predecease your average life expectancy, it would have been better to claim your benefits at an earlier age with reduced benefits.

Converting an employer plan account or Traditional IRA to a Roth IRA is a taxable event. Increased taxable income from the Roth IRA conversion may have several consequences including but not limited to, a need for additional tax withholding or estimated tax payments, the loss of certain tax deductions and credits, and higher taxes on Social Security benefits and higher Medicare premiums. Be sure to consult with a qualified tax advisor before making any decisions regarding your IRA.

Great content here!