What a Business is Actually Worth

The valuation formulas buyers use, the variables that change your multiple, and why most business owners underestimate their asset.

I sat in a meeting last week where someone was about to discover how much money they’d been leaving on the table.

She didn’t know it yet. She had 200 Medicare clients. Maybe 100 ACA. Years of referrals, renewals, relationships.

She knew she had something valuable. She just didn’t know what the number was.

By the end of the hour, she did. This piece is about that number. Not her specific number, but the framework behind it.

Because if you own any kind of book of business — insurance, wealth management, financial planning, any recurring-revenue client base — you probably don’t know what it’s actually worth either.

Most owners don’t. And that gap between what they think they have and what a buyer will actually pay is one of the most expensive blind spots in small business ownership.

The Market Exists. It Just Doesn’t Advertise.

There is an active market for books of business in the insurance and financial services space. Buyers are out there, they have capital, and they buy these books regularly.

Even if you’re not in financial services, these same principles apply to you and your business.

Some are FMOs. Some are larger agencies. Some are private equity-backed consolidators.

They’re not publishing price lists. They’re just quietly buying.

The reason most sellers are shocked by their numbers — in both directions — is that they’ve never looked up what the market actually pays.

They’re sitting on an asset they’ve never appraised. So, let’s do that.

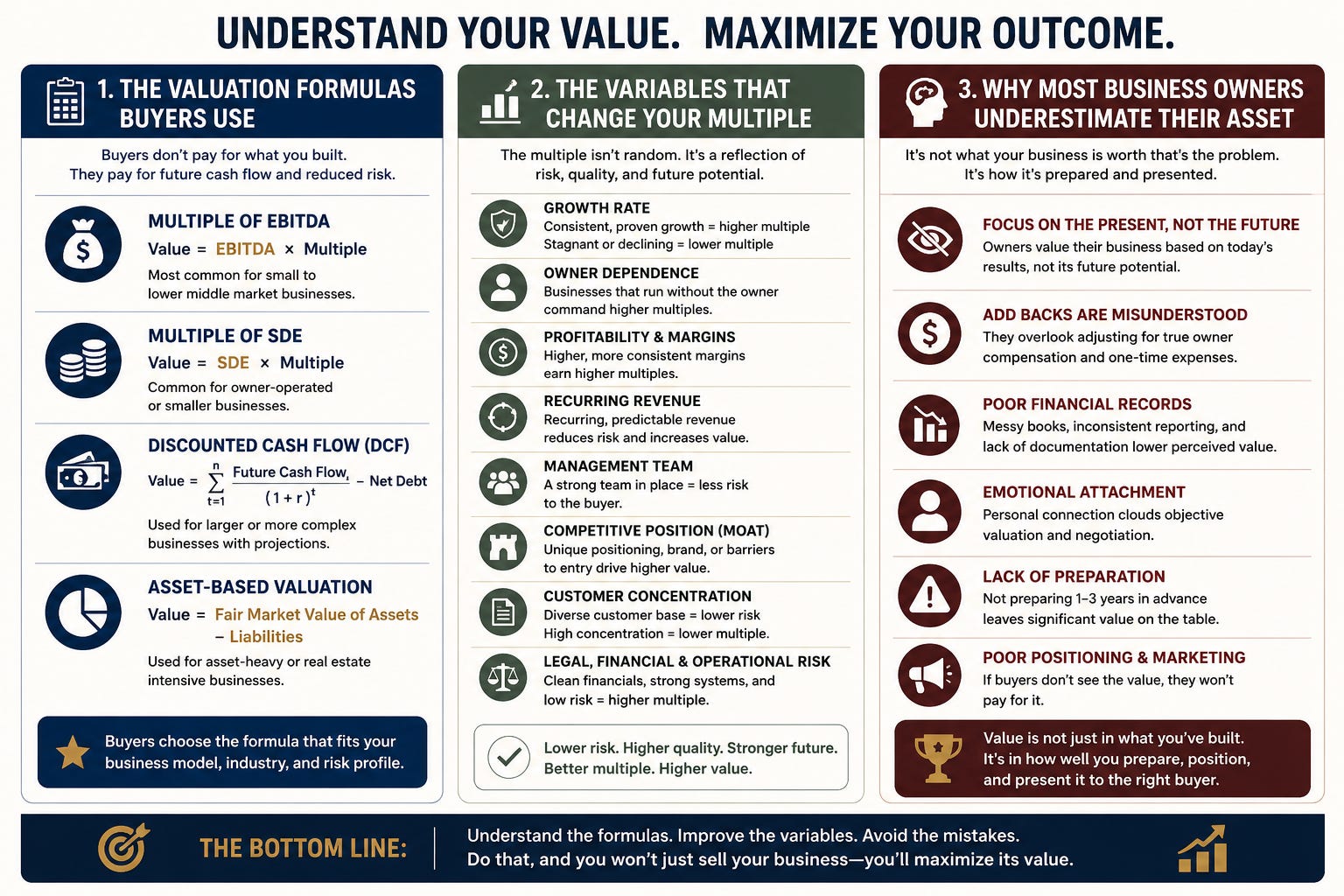

The Valuation Formula is Simple. The Variables Aren’t.

The base formula is straightforward: **annual commission x a multiple**.

What changes the multiple is stickiness. How likely is this client to stay? How painful is it for them to leave? How much work does the buyer have to retain the business?

Here’s how it shakes out across product lines, specifically in the case of our insurance agency client who is looking to retire.

Medicare Advantage clients

These are sticky. Clients don’t change plans often. When they do, it’s usually because an agent helped them. Multiple: 2x to 2.25x annual commission.

ACA (individual marketplace) clients

Moderately sticky, but more price-sensitive. Clients shop around at open enrollment.

Multiple: 1.5x to 2x annual commission.

A clean, well-maintained book with low churn lands at the top of that range.

A book where the agent has been less attentive — closer to 1.5x.

Medicare Supplement clients in Kansas

Higher than Missouri. Closer to 2x. The portability rules in Kansas make the renewal more reliable.

Medicare Supplement clients in Missouri

This one surprises people.

Multiple: 1.5x or less. Possibly well under.

The reason: buyers may move those clients to a different product and, depending on how that goes, may not get paid in year two.

That uncertainty gets priced in immediately.

Small group health (under 50 lives)

Similar to Medicare Advantage. Around 2x annual commission.

Slightly higher in some cases because the relationships are stickier and the renewal conversation is more involved. Buyers like that.

I’m taking you through exhausting detail, so you get the point. Different variables change everything, in every business, when it comes to valuation.

You have to comb through your business in every little detail to understand the nuances of making your business more valuable than it is today.

The Multiple is Not Fixed

The multiples I quoted above are market ranges, not guarantees. Several things move the needle:

Who is staying with the business?

The most important variable. If you’re staying on for 2-3 years as the client-facing person, the multiple goes up.

Buyers know retention is higher when the original agent stays involved. If you want to walk away immediately, expect a haircut.

Every buyer I’ve seen pass on a deal passed on it because the agent wanted out too fast.

What’s the age profile of the clients?

A book full of 68-year-olds is worth more than a book full of 80-year-olds. Younger clients have more years of renewals ahead. Buyers model this.

What’s the concentration risk?

If 40% of your commissions come from one client, that single client is a liability.

Buyers price concentration risk. Diversified businesses get better multiples.

How clean is the compliance picture?

Any complaints, E&O history, or compliance issues will either kill a deal or crater the multiple.

Buyers do not want inherited headaches. A clean record is worth more than people realize.

The Deal Structure Nobody Explains

Most of these transactions are not a wire transfer on day one.

The most common structure is a 3-to-5-year earnout. Here’s how it works:

The buyer agrees on a total price based on the valuation formula. They pay a portion upfront — maybe 50-60% — and the rest is paid out over the earnout period tied to retention.

If the clients stay, you get paid. If they churn, the back end shrinks.

This protects the buyer from paying full price for a book that falls apart. And it aligns the seller’s incentives with retention, which is why buyers strongly prefer sellers who stay involved.

In the best versions of these deals, the seller comes on as a salaried employee during the earnout.

They keep their client relationships, keep writing new business at a commission (typically 25% on new clients, 10% on referrals), and get benefits and retirement contributions through the buyer’s structure.

The earnout is essentially their exit package.

It’s not glamorous. But for a lot of owners who built a good business over 15 years and want to stop worrying about systems and staffing, it’s a very clean way out.

What to Do with This Information

If you own a business of any kind, here’s what to do after reading this article:

Pull up your P&L from the last 12 months. Add up revenues by product or service. Calculate an annual run rate. Then apply the multiples above.

That number is a rough floor. Add to it if your retention is strong, you have repeat customers, or you have great lead flow.

Subtract from it if your book is undocumented, your clients are older, or you want out fast.

That’s the starting point for any real conversation.

You don’t need to sell. You don’t need to merge.

But knowing what you have is different from guessing. And in my experience, the people who know their number make better decisions than the people who don’t.

The business you built is an asset. Treat it like one.

The Best Results Take Time

It takes anywhere from three to four years from the time coffee is planted until it is ready to be harvested.

0-6 months is the seeding process.

1-2 years the plant grows into a bush.

3-4 years flowers appear and the cherries begin to develop.

Because of the dependency on the environment and climate, the average lifecycle is closer to seven years. Once it’s done properly, the plant can be useful for 20-30+ years.

Selling and the succession of a business is the same way. It takes years of diligence and work to exit properly.

For the business to pass on and be successful beyond the sale, it takes years of work and commitment. Just like farming.

As always, drink local and enjoy the good stuff that takes years to produce.

Cheers!

Disclosures:

This blog contains general information that may not be suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this blog will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Revolutionary Wealth LLC does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance. Past performance is no guarantee of future results.

Not associated with or endorsed by the Social Security Administration, Medicare or any other government agency.

Maximizing your Social Security Benefits assumes foreknowledge of your date of death. If as an example you wait to claim a higher monthly benefit amount but predecease your average life expectancy, it would have been better to claim your benefits at an earlier age with reduced benefits.

Converting an employer plan account or Traditional IRA to a Roth IRA is a taxable event. Increased taxable income from the Roth IRA conversion may have several consequences including but not limited to, a need for additional tax withholding or estimated tax payments, the loss of certain tax deductions and credits, and higher taxes on Social Security benefits and higher Medicare premiums. Be sure to consult with a qualified tax advisor before making any decisions regarding your IRA.