The Tax Your Childhood Card Collection Forgot to Warn You About

Collectibles don't get the stock market's 15% tax rate. Here's what the IRS charges instead — and how to plan around it.

There is a specific feeling that collectors know well.

You are cleaning out a closet, or going through a box in your parents’ attic, or helping settle an estate. And you find something. A card. A comic. A piece of memorabilia you completely forgot existed.

You take a photo. You look it up.

And the number on the screen is not what you expected.

This happens more than people realize. A childhood card that came in a pack for a few cents in the late eighties is now worth $10,000.

A comic your dad kept in a bag and board is worth significantly more than that. An inheritance arrives with a piece of collectible history no one bothered to appraise.

Most people in that situation think one of two things: I got lucky. And now I have to pay taxes.

Both are correct. But the taxes are where the story gets interesting — and where most collectors make an assumption that costs them.

They assume collectibles are taxed like stocks. They are not.

The Assumption That Costs Collectors

When most people think about capital gains taxes, they think 15%. That’s the long-term capital gains rate for most Americans — the rate you pay when you sell a stock, a mutual fund, or an ETF that you’ve held for more than a year.

For higher earners it bumps to 20%, but the concept is the same: hold an investment for more than twelve months, pay a preferential rate when you sell.

Collectibles do not get that rate.

Under the tax code, collectibles are their own category. The IRS defines them broadly: art, antiques, coins, stamps, wine, gems, and — yes — trading cards, comic books, and sports memorabilia.

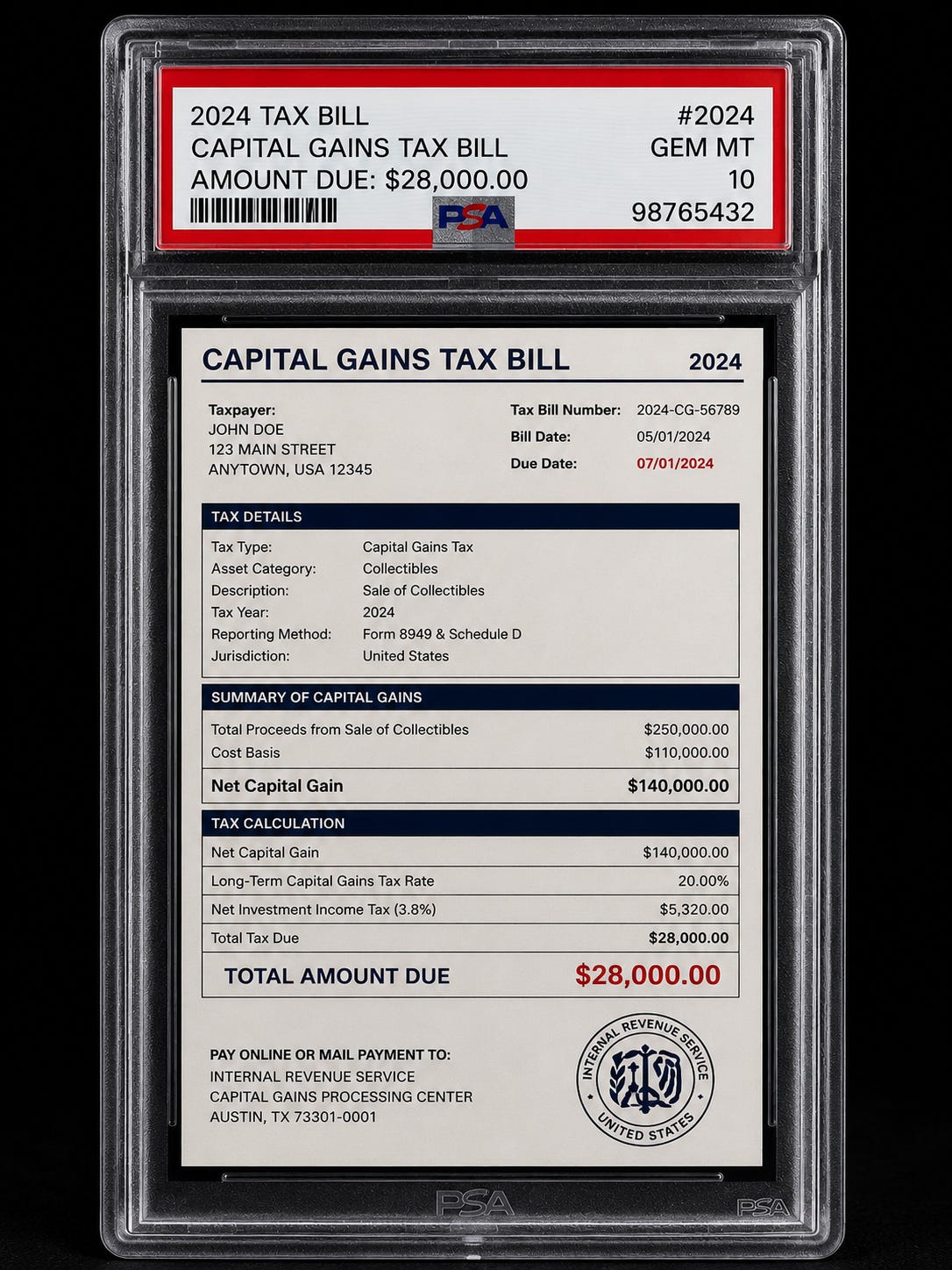

When you sell a collectible you’ve held for more than a year, the maximum federal capital gains rate is 28%.

Not 15%. Not 20%.

Twenty-eight.

On a $10,000 gain, that difference is $1,300 more in federal taxes compared to selling a stock with the same profit. On a $50,000 gain, it’s $6,500.

The number scales, and most collectors never see it coming because their CPA doesn’t specialize in collectibles and no one brought it up at the point of sale.

A dollar lost in taxes you didn’t know about is a dollar gone forever. And this one is worth knowing about before you sell.

Example One: The Childhood Find

You were ten years old. Your mom took you to the drugstore. You spent two dollars on a pack of cards, pulled something you thought looked cool, and stuck it in a shoebox in your closet.

Thirty years later, that card is worth $10,000.

For tax purposes, your cost basis in that card is close to zero. Maybe a few cents. The IRS doesn’t round up on your behalf.

When you sell it, your long-term capital gain is essentially $10,000. At the 28% collectibles rate, your federal tax bill on that find is $2,800.

Most people in that situation are thrilled regardless. It was free money from a shoebox.

But here’s why this matters: if that same $10,000 had come from selling a stock, someone in the 15% long-term capital gains bracket would have paid $1,500.

Same gain. $1,300 more in taxes just because of the asset category.

And that’s before your state adds its own layer. Arkansas taxes capital gains as ordinary income, which means the state gets its cut on top of the federal 28%.

Now imagine that shoebox has fifteen cards in it.

Example Two: The Inherited Collection

This one catches people off guard in a different way, because it involves a tax concept that actually works in your favor — at first.

When you inherit property, the IRS gives you what’s called a step-up in basis. Your cost basis resets to the fair market value of the asset on the date the person passed.

It doesn’t matter what the original owner paid for it. Whatever it was worth when it came to you is what the IRS considers your starting point.

So, if your grandfather bought a card for $50 in 1985, and that card was appraised at $2,000 at the time of his death, your basis is $2,000. Not $50. That step-up erased decades of appreciation from your tax calculation.

It’s one of the most underused planning tools in estate transfers, and it applies to collectibles the same as it does to stocks or real estate.

Here’s where people get tripped up: the step-up covers what you inherited. It does not cover what happens after.

If you hold that card and it climbs from $2,000 to $10,000, the $8,000 increase happened on your watch. When you sell it, that $8,000 gain is taxable. And because it’s a collectible, it’s taxed at 28%.

Federal tax on that $8,000: $2,240.

If you had sold immediately after the step-up — while the value was still $2,000 — the gain would have been zero.

Every month you hold it after inheriting it, you are building a taxable position in an asset class with a higher rate than most people realize.

That is not an argument for selling immediately. Sometimes the right move is to hold.

But it is an argument for knowing exactly what you are holding and what it will cost you when you do decide to sell.

Dealer vs Collector: Why the IRS Cares

The 28% rate applies to collectors — people who buy and hold for personal enjoyment or long-term investment, without making it a regular business activity.

If you are regularly buying and selling cards with the intent to profit, the IRS may classify you as a dealer. Dealers don’t pay capital gains at all.

Their income from card sales is treated as ordinary business income, reported on Schedule C, and subject to self-employment tax on top of their regular rate. For most people reading this, that classification is worse.

The distinction matters because it changes the entire tax picture. A collector sells a $10,000 card and pays 28% on the gain.

A dealer sells the same card and pays their ordinary income rate — potentially 32%, 35%, or 37% — plus 15.3% in self-employment tax on the net profit.

The examples in this article apply to collectors: someone who found a card from childhood, or inherited a piece of a collection, with no pattern of regular buying and selling.

No Whatnot shows. No eBay store. No consistent inventory turnover. Just a card they owned, appreciated, and decided to sell.

If you are actively building an inventory and flipping cards as a side business, the tax picture is a different conversation — and one worth having with a CPA before you file.

What This Means for You

Knowing the rate is step one. Here’s what to do with it.

Document your basis before you sell. If you inherited a collection, get a formal appraisal done as close to the date of death as possible.

That appraisal establishes your step-up and becomes the baseline the IRS will reference if your return is ever questioned.

A formal appraisal from a qualified appraiser is the difference between a clean transaction and an uncomfortable audit conversation three years later.

If the collection came from a childhood purchase, dig up whatever documentation you have. Original receipts, old inventory lists, photos of the collection with timestamps — anything that establishes what you paid.

If your basis is zero, it’s zero. But document that intentionally, not by accident.

Consider the timing of your sale relative to your income. The 28% rate is a ceiling, not a floor. If your ordinary income tax rate is lower than 28% in a given year — say you retired mid-year, sold a business, or had an unusually low income — your collectibles gains may be taxed at your effective rate rather than the full 28%.

Timing a large collectibles sale in a low-income year can reduce the bill meaningfully.

If the collection has significant appreciated value and philanthropy is already part of your plan, donating collectibles to a qualified charity avoids capital gains entirely. You receive a deduction for the fair market value, and the IRS never gets its 28%.

This is not the right move for every situation, but for collectors with large, highly appreciated holdings who are charitably inclined, it is worth running the numbers.

Finally: make sure your CPA has actually handled collectibles before.

This is not a knock-on CPAs. It is an acknowledgment that most tax preparers process W-2s and standard investment accounts.

The collectibles tax rate is a specialty area, and a generalist who isn’t familiar with it may not flag it until after the fact — or may not flag it at all.

Putting the Numbers into Context

When we hear or read 28%, that number can easily go over our heads. Let’s use an example and then put into perspective.

You have a $100,000 card collection that gets sold at a 28% tax rate. That’s $28,000 that the government makes off of YOUR collection appreciating in value.

At the time of this post, you could buy the following cards for $28,000:

Patrick Mahomes 2017 Optic #177 Rated Rookie Autographs - Red /50 PSA 10

Kobe Bryant 1998 Skybox E-X Century #6DG Dunk ‘N Go-Nuts PSA 10

Babe Ruth 1933 Goudey #144 PSA 4

I’m begging you, do everything you can to keep that 28% in your pocket. Hopefully someday you’ll be able to show me a PC card you bought with your compounded tax savings.

See you next time, cheers!

Disclosures:

This blog contains general information that may not be suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this blog will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Revolutionary Wealth LLC does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance. Past performance is no guarantee of future results.