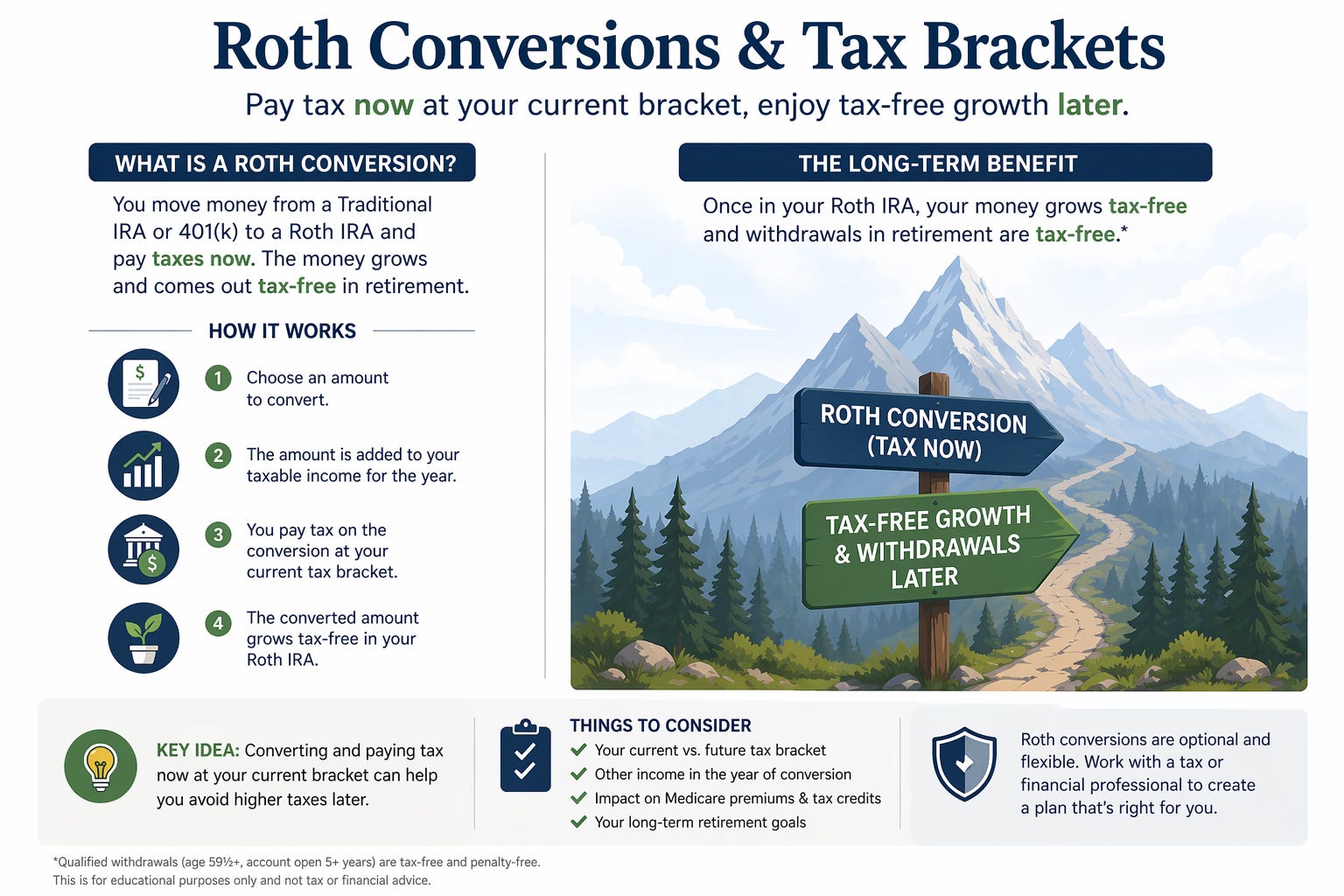

The Roth Conversion Math Nobody Runs For You

The five-year rule, the bracket thresholds, and the math that actually determines whether a Roth conversion pays off.

I have sat across from more retirees than I can count who are afraid of the five-year rule. Almost none of them needed to be.

That fear, and a few other widely repeated half-truths about Roth conversions, is costing people money in two directions at once.

Some avoid conversions they should be doing because they think the rules are working against them.

Others sprint into conversions without understanding the bracket math and end up overpaying by tens of thousands of dollars.

Last week I told you about the couple who converted $340,000 in a single year and walked away with an $80,000 mistake.

This week is the math behind why it happened and what the right approach actually looks like.

The 5-Year Rule Is Not What You Think It Is

Here is the statement I hear constantly: “I cannot touch my Roth money for five years.”

That is partially true, mostly misapplied, and regularly scares people away from conversions they should absolutely be doing.

The 5-year rule has two separate applications and conflating them is where most of the confusion starts.

The first rule applies to Roth IRA earnings. For your earnings to come out completely tax and penalty free, the Roth account needs to have been open for at least five years and you need to be 59.5 or older.

Your contributions are different. You put that money in with after-tax dollars. You can pull your contributions out anytime, tax and penalty free, no five-year clock required.

The second rule applies specifically to Roth conversions. Each conversion has its own five-year clock. If you convert $50,000 from a traditional IRA to Roth and you are under age 59.5, you need to wait five years before you can withdraw that converted amount without a 10% early withdrawal penalty.

This rule exists to prevent people from using Roth conversions as a backdoor early-withdrawal strategy. It was not built to discourage legitimate retirement planning.

Here is the part that matters for almost everyone reading this.

If you are over 59.5, the five-year penalty clock on conversions does not apply to you. You can convert today and access that money tomorrow without the 10% penalty. You will owe income taxes on the conversion when you file, because that is the whole point.

But the rule that people cite as a reason not to convert was never designed for people in their sixties planning their retirement.

For this audience, the five-year conversion rule is a non-factor. Stop letting a penalty that does not apply to you make your retirement decisions.

The 12% Bracket Math Nobody Wants to Talk About

For most pre-retirees and retirees, the 12% federal tax bracket in 2026 covers taxable income from roughly $12,400 to $50,400 for single filers, and up to $100,800 for married couples filing jointly.

That sounds like conversion room. And it is. But here is what the numbers actually look like when you map out the lifetime tax savings.

Say you are 62 with $180,000 sitting in a traditional IRA. You fill up the 12% bracket over a few years by converting that money. You pay 12% on it now instead of a potentially higher rate later.

How much do you actually save?

At best, if every dollar you converted would have otherwise been taxed at 22%, you saved 10 cents on every dollar. On $180,000, that is $18,000 in gross tax savings. Before you account for the opportunity cost of paying taxes years before they were due.

Stretched over a 20-year retirement with reasonable growth projections, the lifetime tax savings from filling the 12% bracket typically lands somewhere in the high five figures. Sometimes just over $100,000. Sometimes less, depending on your situation.

That is meaningful. It is not a retirement transformation. And it only makes sense at all if you actually expect to be in a higher bracket in retirement than you are today.

For many people with modest retirement income and required minimum distributions that stay comfortably under $50,000 per year, the 12% bracket conversions do not move the needle the way the internet suggests. The math closes narrowly if it closes at all.

The projection has to close. Do not let a strategy that sounds right shortcut the actual calculation.

The Brackets Actually Worth Filling

The real leverage in Roth conversions lives in the 22% and 24% tax brackets.

Here is why.

At those income levels, your portfolio is large enough that required minimum distributions become a genuine future problem. The IRS requires you to start withdrawing money from your pre-tax retirement accounts at age 73 or 75, whether you want to or not. These withdrawals are calculated as a percentage of your account balance each year, and that percentage increases as you get older.

If you have $800,000 in a traditional IRA at 73, your first required minimum distribution is roughly $29,000. By 80, your balance has likely grown and your distribution percentage has increased.

By 85, you are looking at mandatory withdrawals that can push a retirement income that looked manageable into the 24% or 32% bracket. The distributions do not slow down. They compound the problem.

Higher required minimum distributions also trigger two secondary consequences that most people do not see coming until they are already in them.

First, they can increase the portion of your Social Security benefit that is taxable, up to 85% of your benefit amount.

Second, they can push your income above the Medicare IRMAA threshold, which adds surcharges to your Part B and Part D premiums. In 2026, a married couple with income above $206,000 pays an additional $838 per month in Medicare surcharges.

That is more than $10,000 per year in costs that did not exist at a lower income level.

Filling up the 22% and 24% brackets today, before required minimum distributions force the issue, is a genuine strategy with real math behind it. You are paying at a known rate now to avoid a higher rate later on a larger account balance.

Spread across a 15-to-20-year retirement, strategic conversions into those brackets can protect $400,000 to $900,000 or more in combined tax exposure, Medicare surcharges, and Social Security taxability, depending on your portfolio and timeline.

That is the Roth conversion conversation worth having.

The $200,000 Portfolio Threshold, Revisited

Last week I introduced a starting point I use in my practice: Roth conversions are best suited for portfolios over $200,000 in pre-tax accounts for people 65 and younger.

The bracket math is exactly why.

If you have $200,000 or less in pre-tax accounts and you are over 65, your required minimum distributions at 73 will be modest. On a $180,000 balance, your first distribution at 73 is roughly $6,900.

That number stays manageable for most of retirement. There is no bracket-push problem to solve, and no Medicare surcharge exposure to protect against. The urgency that generic advice creates simply does not exist.

But if you have $600,000 or $800,000 in a traditional IRA at 62, the math looks completely different. Your required minimum distribution at 75 on $800,000 is roughly $29,000. That is also assuming your account hasn’t grown in thirteen years.

If you also have Social Security income and other retirement income on top of that, the combined total may be pushing you toward the 24% bracket or higher. And that distribution grows every year.

That is the tax risk Roth conversions are designed to solve. Not the risk of “rates might go up someday.” The specific, calculable risk of mandatory distributions stacking on top of everything else you have coming in.

The threshold matters because it is a quick read on whether the problem actually exists for you. Below $200,000 at 65 or older, there is usually no fire to put out. Above $200,000 at 65 or younger, there usually is.

Get the projection. The number is specific to you.

Margin Matters

A coffee shop runs on a 3 to 7 percent net margin. That is not a lot of room.

The owners who protect those margins are not doing it by selling more lattes. They are doing it by adding higher margin products like muffins, t-shirts, etc.

Retirement planning that is optimized for financial confidence, it designed the same way. The little things become big things.

1-2% annually recovered from tax planning and other strategies is the equivalent to protecting your “margin” when bumps in the road come your way.

Remove only and just from your vocabulary. It’s “only” 2% back on your money until that 2% a year is the difference between running out of money and living with dignity later on in life.

Plan for the road ahead, buy the muffin at the shop. You’ll both be grateful that you did.

See you next time, cheers!

Disclosures:

This blog contains general information that may not be suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this blog will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Revolutionary Wealth LLC does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance. Past performance is no guarantee of future results.

Not associated with or endorsed by the Social Security Administration, Medicare or any other government agency.

Maximizing your Social Security Benefits assumes foreknowledge of your date of death. If as an example you wait to claim a higher monthly benefit amount but predecease your average life expectancy, it would have been better to claim your benefits at an earlier age with reduced benefits.

Converting an employer plan account or Traditional IRA to a Roth IRA is a taxable event. Increased taxable income from the Roth IRA conversion may have several consequences including but not limited to, a need for additional tax withholding or estimated tax payments, the loss of certain tax deductions and credits, and higher taxes on Social Security benefits and higher Medicare premiums. Be sure to consult with a qualified tax advisor before making any decisions regarding your IRA.