She Waited 11 Months to Access $700,000 That Was Already Hers

Arkansas probate can freeze your estate for nearly a year and cost your family tens of thousands of dollars. Here's what to do before it's too late.

A while back, a referral called our office. She had heard we helped people with estate planning. So, I sat down with her on a Zoom call — her, a widow in her early sixties, composed in the way that people get when they have had eleven months to sit with something painful and work through it alone.

She wasn’t panicking. She wasn’t overwhelmed. She was patient in the way that only comes from having already survived the worst of it.

Her husband had passed while they were still legally married. They had been separated for several years, but the divorce was never finalized. No one had updated the deed to the house during the separation.

No one had retitled the financial accounts. In the chaos of trying to untangle a marriage, that paperwork almost always falls to the bottom of the list. And when it stays there long enough, a death turns it into someone else’s emergency.

Because her name wasn’t on the deed, the state of Arkansas stepped in.

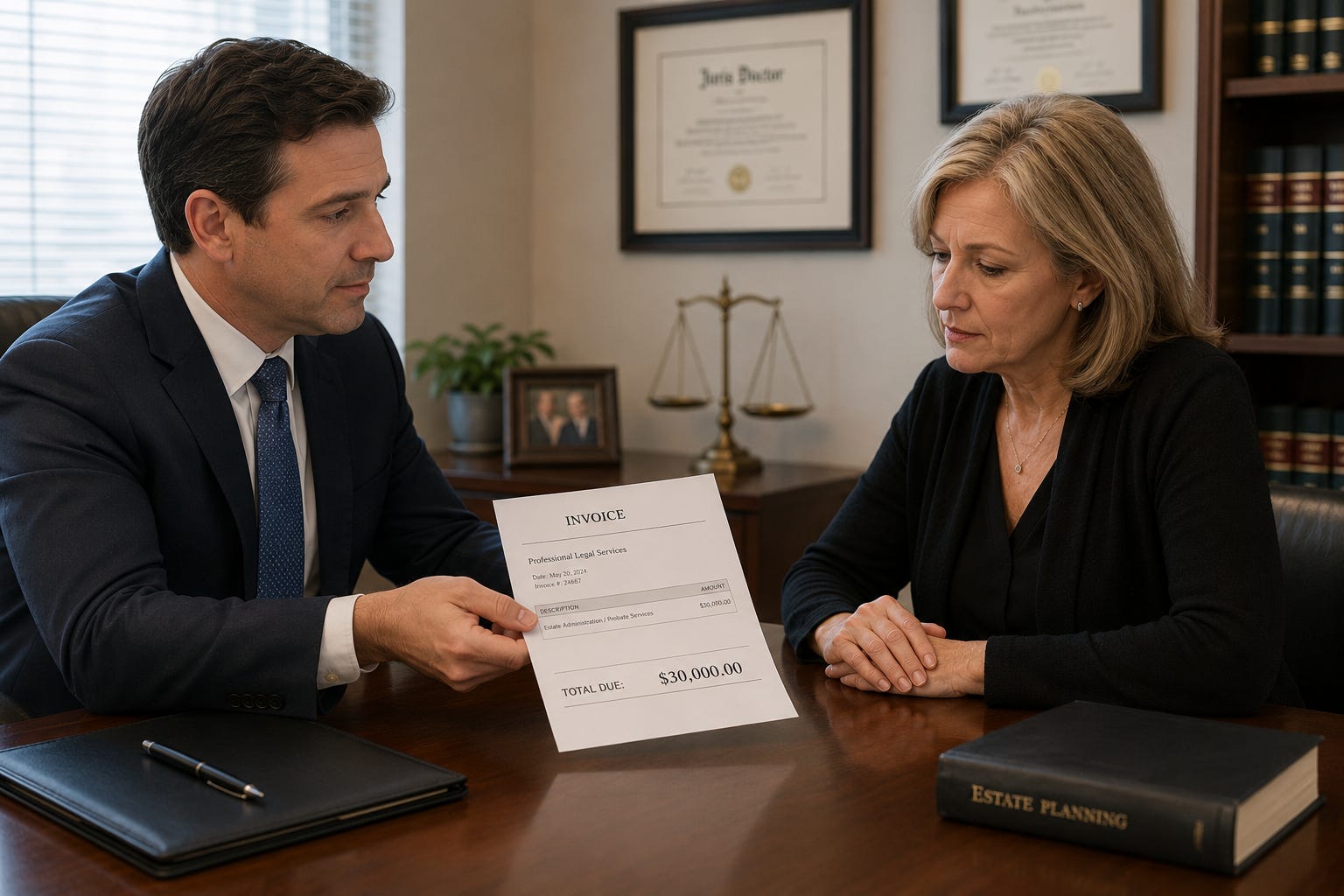

Approximately $700,000 worth of assets that she had spent decades helping to build were frozen inside the Arkansas probate system.

The final bill to get those assets released: $30,000 in attorney fees.

She didn’t do anything wrong. She didn’t miss a law. She fell into the most common estate planning trap in Arkansas, and almost no one warned her it was there.

The Trap is the Title, Not the Marriage

Most people assume marriage is protection. They assume that if their name is on a marriage certificate, they’re covered. In many cases that’s a reasonable assumption.

Joint tenancy with right of survivorship, proper beneficiary designations, assets titled in both names — these things can pass cleanly to a surviving spouse without touching probate at all.

But the trap is this: Arkansas probate law doesn’t care about the marriage. It cares about the title.

If an asset is titled in your spouse’s name alone, that asset goes through probate court when they die. It doesn’t matter that you were married for 32 years.

It doesn’t matter that you helped pay for it. It doesn’t matter that everyone in the room agrees it was yours. The court moves on paperwork, not on context.

And in a separation, where most couples are managing the emotional weight of the day rather than updating estate documents, that paperwork almost never gets fixed.

Life moves forward. The deed stays the same.

That’s the trap. And it catches people who did everything else right.

What Most People Get Wrong First

Here’s the other piece no one explains clearly enough: a will does not avoid probate.

Most people in Arkansas assume that having a valid will means their estate is handled. A will guides who receives your assets, but it does not automatically transfer ownership.

It still has to be filed with the probate clerk. It still gets administered through probate court. The will tells the court who gets what. The court still runs the process.

If there is no will, Arkansas probate laws decide the heirs through intestacy — which means the state makes decisions that should have been yours.

So, when someone says, “I’ve got a will, my family is taken care of,” I try to say this gently: a will is better than nothing, but it is not a plan to avoid probate.

It’s a roadmap for a process you were hoping to skip.

What Arkansas Probate Actually Does to Your Family

The probate process in Arkansas runs in four phases, and your family does not get to skip any of them.

Phase one: someone files a petition with the circuit court. The court appoints a personal representative — typically the surviving spouse or a named executor — to manage the estate.

Phase two: the court publishes a notice to creditors. In Arkansas, creditors have a minimum of three to four months to file claims against the estate. That clock starts from the date of publication, not the date of death. While it runs, your family cannot access or distribute the frozen assets. They wait.

Phase three: the personal representative inventories every asset in the estate, pays valid debts, and files any required state and federal tax returns. Every missing document, every complication in the titling structure, every dispute adds weeks.

Phase four: whatever remains gets distributed to beneficiaries, subject to court approval. Then it’s done.

Under the best circumstances, this process takes six to twelve months. Under complicated circumstances — a separated couple, assets titled in one name, a surviving spouse establishing her legal right to property she helped acquire — it stretches well past that. Eighteen months is not unusual.

Attorney fees in Arkansas are typically calculated as a percentage of the gross probate estate. On a $700,000 estate, a standard fee lands between $21,000 and $28,000.

Add court filing costs, publication fees, and the added complexity of the separation, and you arrive at $30,000.

There’s one more cost that most people don’t think about until it happens: privacy.

Probate filings in Arkansas are public record. Your assets, your debts, and your beneficiaries become available to anyone who looks. If that concerns you — and it should — the trust conversation becomes even more important.

That’s not a mistake or a scam. That’s the system doing exactly what it was built to do.

The only mistake was not having a plan in place before it was needed.

The Partial Fixes - and Where They Fall Short

When I walk people through this, the first thing most of them say is some version of: “Can’t I just put my spouse on everything?”

You can. And you should start there. Joint titling and beneficiary designations solve a large portion of the exposure. For married couples, Arkansas recognizes Tenancy by the Entirety, which automatically transfers marital property to the surviving spouse when the first spouse passes.

Payable-on-death designations on bank accounts and transfer-on-death designations on brokerage accounts accomplish the same thing for those assets — they pass directly to the named beneficiary without going through probate court at all.

These tools work. They’re underused, and they’re free. If you have not reviewed your beneficiary designations recently, that’s the first call to make.

But they don’t solve all of it.

If you and your spouse own a home with right of survivorship, it passes to the survivor cleanly. Good. But when the second spouse passes, both names are off the deed.

Whoever inherits that property may be heading straight into probate anyway. You delayed the problem. You didn’t eliminate it.

More importantly, adding a child’s name to a deed to “make it easier later” creates new vulnerabilities. It can trigger gift tax exposure, complicate the capital gains calculation when the property is sold, and expose your home to that child’s creditors or a divorce proceeding.

People try to outmaneuver the system without understanding what the system is actually tracking.

The system tracks titles. Partial fixes help. But they don’t finish the job.

What Actually Bypasses Probate

A revocable living trust does not go through probate.

Assets held inside a trust pass directly to your named beneficiaries. The court is not involved.

There is no creditor notice period. There is no attorney calculating a percentage of your gross estate. There is no eleven months. There is no $30,000.

Here’s how it works in plain language. You create the trust during your lifetime and fund it by retitling your assets into the trust’s name.

Your home, your investment accounts, your retirement accounts, any real property — they become assets of the trust rather than assets in your individual name.

You remain the trustee. You control everything exactly as you did before.

When you pass, the successor trustee you named distributes the assets to your beneficiaries according to your written instructions. No court required. No delay. No percentage off the top. No public filing.

On a $700,000 estate, a well-structured revocable trust in Arkansas typically costs between $3,000 and $5,000 to set up. One time. Compare that to the $30,000 that client paid to recover assets from a process that should never have been necessary.

That $30,000 doesn’t come back. A dollar lost in probate is a dollar gone forever. Unlike taxes, this one is completely optional.

One trust structure solves four problems at once: it avoids probate, keeps your estate private, protects against court challenges, and gives you a living document you can update as your life changes.

If you remarry, update it. If a beneficiary passes before you, update it. If your assets shift, update it. You’re in control for as long as you’re alive.

That, ladies and gentlemen, is what it looks like when a planning tool solves two, three, sometimes four problems simultaneously.

The Part That Surprised Her Most

Here’s what caught that client off guard, and what catches almost everyone I walk through this with.

Her husband’s estate was not complicated.

There was no business to dissolve. No creditor disputes. No contested will. No blended family fighting over who gets what.

Just a separated couple, some real estate, some accounts, and a titling structure that nobody thought to update while everyone was busy living through the separation.

And it still cost her $30,000 and eleven months of her life.

She told me at the end of our call that what hurt most was not the money. The money she could eventually account for and move past.

She said the hardest part was calling that attorney every few weeks and being told, again, that the process was still moving. That she just had to wait. That there was nothing she could do to speed it up.

That her hands were tied.

A trust means your family’s hands are not tied.

The probate system in Arkansas is not broken. It is doing exactly what the legislature built it to do.

But it was built for people who didn’t plan ahead. You are reading this. That means you have time.

What You Can Do This Week

Pull up your three largest assets: your home, your investment and retirement accounts, and any real property you own.

For each one, ask two questions. How is this asset titled? Is there a valid, current beneficiary designation on file?

If the answer to either question is no, that asset has probate exposure.

The next call you make should be to an estate planning attorney who has handled Arkansas probate cases before — someone who knows where the traps are built into the system.

That’s exactly why we built Blueprint Business and Tax Advisors. We have an estate planning attorney on staff who handles the full implementation — drafting the documents, walking you through the funding process, and notarizing everything so nothing gets left undone.

We built it to be cost effective by design. The national average for a trust setup runs around $5,000. We charge our financial planning clients $2,000.

Same attorney. Same documents. A fraction of the cost, because we believe the plan should not be the thing that stops people from getting protected.

Plus, we invest in cutting edge technology that allows you to get your estate plan in place in hours, not months.

If you are a financial planning client or want to become one, reach out. We will handle it.

Eleven months in probate and $30,000 in fees. Or 2 hours and $2,000.

Grab your coffee. Pull out your documents. Make the call.

Your family deserves to make the decisions that are theirs to make. Not the state of Arkansas.

Disclosures:

This blog contains general information that may not be suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this blog will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Revolutionary Wealth LLC does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance. Past performance is no guarantee of future results.

Not associated with or endorsed by the Social Security Administration, Medicare or any other government agency.

Maximizing your Social Security Benefits assumes foreknowledge of your date of death. If as an example you wait to claim a higher monthly benefit amount but predecease your average life expectancy, it would have been better to claim your benefits at an earlier age with reduced benefits.

Converting an employer plan account or Traditional IRA to a Roth IRA is a taxable event. Increased taxable income from the Roth IRA conversion may have several consequences including but not limited to, a need for additional tax withholding or estimated tax payments, the loss of certain tax deductions and credits, and higher taxes on Social Security benefits and higher Medicare premiums. Be sure to consult with a qualified tax advisor before making any decisions regarding your IRA.